Price Ceiling:keeps prices from getting too high. ex: rent control

Consequences of price ceiling

1. lower prices for some consumers

2shortage

3 long lines for buyers

4 illegal sales above equilibrium price

Elastic Demand- demand that is very sensitive to a change in price. product is not a necessity and there are available substitutes

Ex: steak, pork

E>1

Inelastic Demand: demand that is not sensitive to a change in demand.

the product is a necessity and there are few to no substitutes

Ex: Milk, insulin

E<1

Unit Elastic on Unitary Elastic Demand-

measure of how consumers react in a change in price.

E=1

PED FORMULAS:

Step 1 quantity New-Old

Old

Step 2 price New- old

old

Step 3:% ⃤ change in quantity

%△ change in price

Demand is - the quantities that people are willing and able to buy at various prices

The Law of Demand- there is an inverse relationship between price and quantity demanded

What causes a change in quantity demanded?

⃤ in price

What causes a change in demand?

⃤ in number of buyers

population: mass buying products from sellers

⃤ in buyers taste

preference: a new trend or craze buyers want

⃤ in income

inferior goods- goods that people buy less of when their income rises

normal goods- goods people buy when their income increases.

⃤ in price of related goods

substitute: goods that serve roughly the same purpose to buyers

complimentary goods: goods that are often consumed together

⃤ in expectations

goods that people buy when their income increases

Difference between Micro and Macro economics Macroeconomics- the study of economics as a whole. (BIG PICTURE) Microeconomics-the study of individual or specific units of the economy. (SMALL PICTURE) Positive vs Normative Economics Positive: claims to describe the world as is. (FACTS) ex: minimum wage laws cause unemployment. Normative: claims that attempt to say how the world should be (OPINION) ex: the government should raise min wage. Want vs Needs Want: desire, optional (cellphone, tv) Need: necessity to survive (water, food, air) Scarcity vs Shortage Scarcity: problem that all societies face, how to satisfy UNLIMITED wants with LIMITED resources? Shortage: Quantity Demand > Quantity Supply Goods vs Services Goods : tangentable object. E1: consumer goods, (goods intended for final use by consumer) Ipod, Tv, Barbie E2: Capital Goods (items used to create other goods) plastic,wood, Services: action performed by one person for another. Factors of Production 1.Land : Natural resources

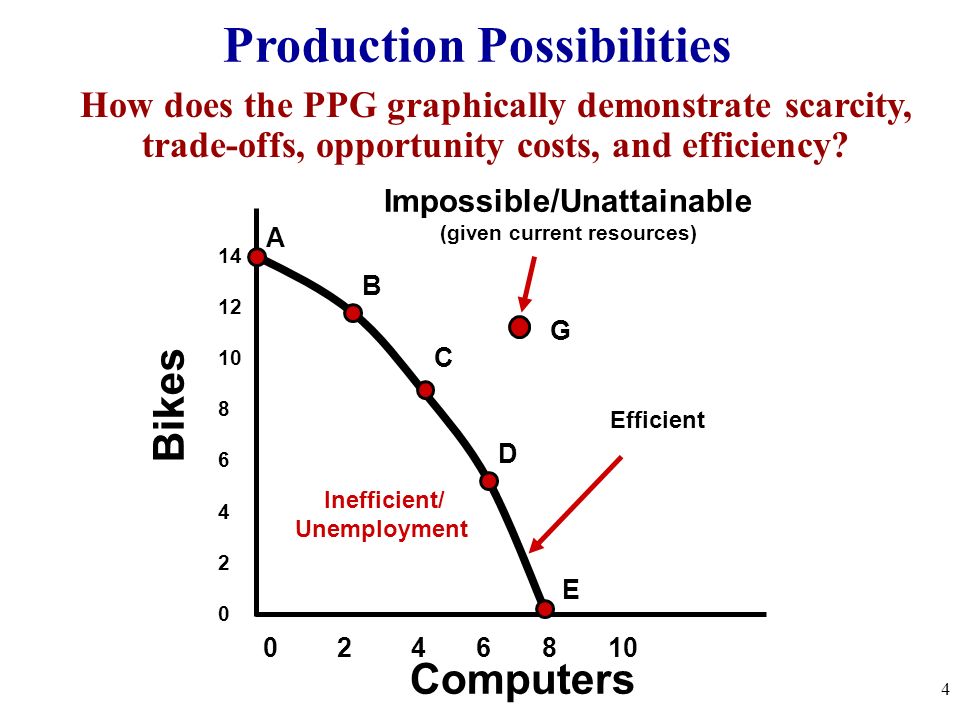

2.Labor: the workforce 3.Capital: Human Capital: Knowlege and skills a worker gains through education and experience Physical Capital: human-made objects used to create other goods and services. 4.Entrepreneurship: inventive and risk-taking. Opportunity Costs: the most desirable alternative given up by people when making a decision. tradeoffs: alternative decisions that people make when faced with an economic dilemma.

Price floor- legal minimum price meant to help sellers4 consequences1 higher product price2 a surplus3 higher taxes or higher government debt if the government buys a surplus4 waste

Price floor- legal minimum price meant to help sellers4 consequences1 higher product price2 a surplus3 higher taxes or higher government debt if the government buys a surplus4 waste

/what-is-balance-of-payments-components-and-deficit-3306278-Final1-c67946023d0f4cdcb7e7794de02947bc.png)